- Blogs

- Posted

The Daft.ie report is wrong: tighter building regs don’t hurt profits

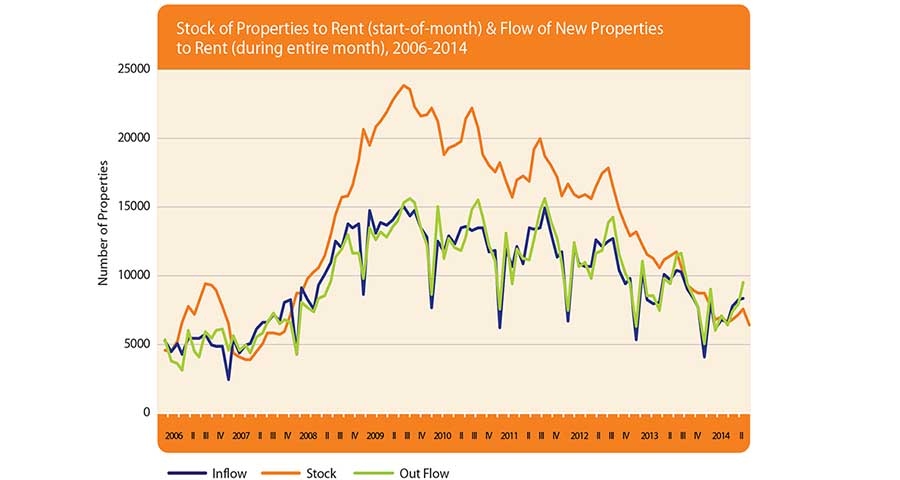

Leading Irish property portal Daft.ie’s latest quarterly rental report was published this week, and included an assertion on the link between construction and planning requirements and the profitability of development – an assertion our editor felt Jeff Colley compelled to debunk.

While I of course sympathise with students and indeed anyone else who may be struggling to find affordable accommodation, I have to respectfully disagree with the assertion the latest Daft.ie quarterly rental report that “As building regulations and planning costs grow, profit margins in the sector have fallen, impinging the appetite of lenders to lend and of investors to invest. Fewer homes are then built.” This is a red herring. Granted, commencement notices have fallen as an apparent consequence of the Building Control Amendment Regulations, but that's an extraordinary circumstance, and normal service will resume eventually – even if the state has to first relent and amend the regulations.

I think most Irish people know why the banks haven't been lending since the economy crashed, and it's nothing to do with new building regulations. Besides, where's the data to indicate that banks have been lending freely on existing buildings, which – other than where an upgrade or extension's involved – aren't affected by tightening building regs and planning requirements?

Higher construction and planning requirements don't make development less profitable as a general principle. They instead cause land prices to fall. I had a meeting recently with one of Ireland's most prolific developers, who confirmed that when he's bidding on land he factors in the higher construction costs and bids less for the land. The exception is where a developer is sitting on a land bank. In that circumstance, they do stand to lose out a little, if they had expected construction costs to be lower, and consequently bid too much for the land and then sat on it. But it's hard to feel sympathy here, given that developers sitting on land banks are one of the main causes of house price inflation. Besides, building regulations have been progressively improving since the Building Control Act came in over 20 years ago, so it’s a foolish developer who bought land without factoring in the risk of regulations tightening further by the time they get around to building.

But even a developer sitting on a land bank won't necessarily see reduced profits when they eventually build, if the market's willing to pay more for the higher quality buildings that tighter regulations demand – and Ronan Lyons et al have demonstrated that in terms of energy efficiency, A rated homes are currently fetching a sale price premium of almost 10% compared to a similar D-rated home. This doesn't mean house prices in general will rise. If new homes start to fetch a premium, it may devalue existing homes a little, but that impact is likely to be very marginal, as the number of new homes on the market will only be a fraction of the number of existing homes, meaning any devaluation would be spread (though perhaps not evenly) across a much larger number of properties.

It's also worth bearing in mind that the reputation of the construction sector has taken a battering, and with the likes of Priory Hall and the pyrites problem still fresh in the mind, confidence in the industry's output during the boom is understandably low. New housing must be better built to restore consumer confidence in the industry's product.

And from an investor's point of view, is it not preferable if the price of a given house reflects the quality of construction more than land value? Surely such a building is more likely to retain its value than a poor quality building which has attracted a premium because of artificially high land prices?