Jason Walsh

Jason Walsh

Green Loans

For the first time in several years, 2007 will see a budget deficit in Ireland so the question must be asked: where does this leave state aid for sustainable building? Construct Ireland’s Jeff Colley and Jason Walsh propose a new approach to improving the energy efficiency of existing homes that might even fix a few of the difficulties seen in the last eighteen monthsFirst implemented last year, Sustainable Energy Ireland's Greener Homes grant aid scheme has been a central plank of the government's strategy to both reduce the carbon emissions of Irish houses and stimulate growth in the renewable energy sector. Designed to allow homeowners to improve the energy efficiency of their homes, Greener Homes and other similar schemes such as the House of Tomorrow programme, have been instrumental in moving from confusion about energy matters to actually doing something about energy use in Irish buildings.

There is no doubt that both schemes have played a role in putting Ireland on the map with regard to sustainability. Nevertheless, in a very real sense both schemes, and the Greener Homes scheme in particular have been victims of their own success.

Since its inception in April 2006 the Greener Homes scheme alone has seen 16,000 successful applications, from a total fund of e47 million. The original fund of e27 million - intended to grant fund renewables over 5 years - was exhausted within a matter of months, with Brian Cowen announcing a further e20 million allocation in December 2006. This e47 million has now been spent.

On 3 September, 2007, Eamon Ryan, Minister for Communications, Energy and Natural Resources and Green Party TD, announced that the scheme was being halted, albeit temporarily, while an assessment on future need was performed. "Greener Homes has fulfilled its objectives. Rather than concluding the scheme, however, I have decided that a new phase with revised terms and conditions is necessary to continue this good work. I will be securing additional funding for this new phase via the supplementary estimates process when the Dáil resumes," said Ryan. Tellingly, in contrast to previous government announcements on the first phase of Greener Homes, there was no mention of the total amount of money ring fenced for the second phase.

While the minister's objective may well be to secure additional funding for Greener Homes and other energy efficiency schemes one clear obstacle is likely to stand in his path: the Department of Finance.

A report issued on 4 September saw Ireland's budget deficit rise to e2.88 billion, calling into question the government's will to continue public spending. Rossa White, economist with Davy Stockbrokers, told the Reuters news agency: "Expenditure is running slightly ahead of target. It increased by 19.8 per cent in the first eight months compared with a forecast of 17.4 per cent." This clearly indicates the possibility of – and likely desire for in the business community – a round of belt-tightening.

Of course, the country is far from poor. Last year, for example, the state finances ran at a surplus of e203 million. Nonetheless, it is quite possible that the combination of a budget deficit, a significant slowdown in the construction sector and ever-increasing international competition in other industries with a significant foothold in Ireland, such as software development and pharmaceuticals, from Eastern Europe, India and China, will see a new era of parsimony ushered in under the guise of 'prudence' and risk-aversion.

In these circumstances cuts are likely to be made where they can be and schemes such as Greener Homes may well appear, to the Department of Finance at least, to be ripe for the picking. Still, it is clear at this early stage is that some action will need to be taken to support the renewable energy and broader energy efficiency sectors. Homeowners are not likely to respond well to the rug being pulled-out from beneath their feet, while the industry itself is already beginning to make its displeasure heard. A recent report in the Irish Examiner stated that: "Jobs in the sustainable energy sector have been put at risk by Energy Minister Eamon Ryan’s decision to close the Greener Homes funding programme until October."1

Improved equity

In light of all of the above one possible solution is to replace Greener Homes with a commercial loan which some industry figures and commentators feel could, if properly implemented, significantly improve on Greener Homes' record.

The mechanics of the proposed scheme are relatively straightforward. Each applicant should receive two Building Energy Rating (BER) assessments of their house, one at the time of application and a second after the improvements have been made.

The results of the initial survey should not only provide a clear BER for the house, for example 'C', but inform the process by which this rating can be improved to a 'B', or preferably an 'A'. The loan would be made by a lending institution, either a Credit Union or a commercial lender, on the basis of the improvement sought.

Here the state should step in, perhaps by paying for the BERs. This in itself may be the full extent of government support for the plan, thus reducing the burden on public finances while the loan itself should be effectively 'income neutral' for the borrower as a result of the energy savings in the dwelling.

Testing would need to be performed in an impartial manner in order to ensure proper compliance: "The aim should be to create a core of independent expert analysts," says economist Richard Douthwaite.

Douthwaite argues that in order to preserve their independence these analysts should not be civil servants or in the direct pay of the industry: "The government should pay for them directly. They would act more like insurance brokers [than civil servants] but they wouldn't be selling anything," he says. Indeed, the advisors' main task would be not only to certify dwellings but also to suggest a suitable methodology for improving any given house, such as through energy-saving techniques such as better insulation and, once everything practical has been done to reduce energy consumption, through the installation of low or no-fuel cost energy sources such as renewable energy systems.

Some questions will need to be asked about the idea of creating a legion of state-funded 'experts' paid from the public purse, as well as how to ensure that knowledgeable and disinterested people who can provide actually useful information take up the posts. Indeed, the recent British experience of so-called 'Home Inspector' energy assessors has been roundly criticised as a failure in the press as being essentially a waste of time and money. This indicates a possible role for the already existing energy agencies as they already possess the necessary expertise and there would be no duplication of services.

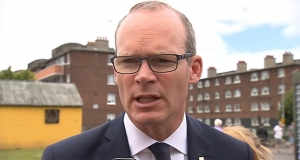

Energy minister Eamon Ryan pictured at a meeting with Construct Ireland in the summer. Ryan is currently looking at the proposal for green loans put to him by Construct Ireland

Douthwaite argues that a professional presence is paramount for such a scheme's survival: "They should also do a final check for BER compliance – people are concerned about cowboys, they would like to go to a professional for advice."

Involving independent energy experts in the decision of how to reduce energy costs would avoid a serious criticism of the Greener Homes scheme: the focus on particular technologies has led to confusion, market distortion and, in some cases, failure. For instance, by concentrating on heating systems Greener Homes has often put the cart before the horse and failed to guarantee any significant cost savings for consumers.

As an analogy, when faced with a leaky bucket it is more sensible to plug the leak than to continually refill the bucket. Likewise, problems with substandard insulation and air infiltration in Irish buildings need to be addressed before moving toward the use of renewable energy for heating and cooling. Installing a new heating system - however green it may be - in an energy inefficient building is effectively continuously filling the bucket.

As the Department of Communications, Energy and Natural Resources tacitly admits, the Greener Homes scheme has been enormously oversubscribed. This sudden surge of demand led last year for instance to talk of a wood pellet fuel shortage, which duly cast doubt wrongfully into many people’s minds about whether they should invest in pellet stoves or boilers if they thought the pellets mightn’t be there to meet their demand.

As the exhaustion of the Greener homes’ e47 million fund in little more than a year and a third demonstrates, it is difficult to predict the level of demand when planning grants programmes, which can lead to significant over spending.

Another problem with the scheme was a lack of criteria for installers, which has in many cases led to poor installations. Relatedly, consumers have been expected to make their own decisions without getting independent advice that addresses the specifics of their particular dwelling or occupancy patterns. There have doubtless been many occasions where people chose the wrong option for their needs due to price, instinctively buying cheaper systems in terms of capital costs rather than in terms of running costs over the lifetime of the system. Some have argued that people have been misled by salesmen, often supplying the wrong technology for the homeowner’s individual needs and delivering poor service.

It is also questionable that the state should determine how heavily subsidised one technology is over another and, indeed, if the state has the expertise to make such judgements. If nothing else, this does seem to run counter to the prevailing free-market ethos of contemporary Irish economic policy. Whatever one's political position on such matters, one should ask whether the state should, for example, fund one technology more heavily than another, and exclude technologies such as heat recovery ventilation entirely? How are such decisions made, by whom and according to what criteria?

Grant me strength

Consulting engineer Xavier Dubuisson is rather more enthusiastic about the record of SEI's various grant schemes but argues that they have done their job and that it's now time to move on to something new. Now the principal of XD Consulting, Dubuisson is a former manager of SEI’s Renewable Energy Information Office and was instrumental in the setting up of the Greener Homes scheme.

For Dubuisson, a loan scheme is an ideal way to address the disappearance of grant aid: "My concern at this stage is that if you replaced the Greener Homes scheme tomorrow without a 'soft loan' it would be too much of a shock to the system."

He argues that the interest rate on the loan should be reduced relative to how much of an improvement is made in the BER: "If the rates are fixed at the right level it would work. I would like to see a link with the drop in energy use. If you're moving from B3 to B2 you might get, say, five per cent but for a move from B3 to A1 you'd get a better rate."

Dubuisson is adamant that the Greener Homes scheme performed its task admirably but he is not blind to its deficiencies: "The grant's main effect was to prime the market – that was the general aim, both on the demand side and the supply side. Renewable energy was a very small sector [before the grant] and now it's much larger.

"It's also been an important factor in rallying SEI. Everyone put in an enormous amount of goodwill. It put SEI on a level it wasn't at before. It also put Ireland on the European map – companies in countries like Germany are now looking at Ireland.

"On the negative side, basically it was set at too high a level, certainly for pellet boilers and heat pumps, to the point where some boilers were [significantly] cheaper to manufacture than the grant. Lower quality boilers were flogged [and] the renewable market attracted cowboys. The fact that the grant has [since] been reduced could have a positive effect in terms of cooling the market and going back to 'organic' growth."

Dubuisson says that some form of official support for the renewable sector is vital and that in the present circumstances a loan could be the appropriate measure. He also supports the idea of the Credit Unions and other alternative organisations being central to such a scheme: "I think the Credit Unions are well-known community-based organisations. You could also have the utility companies involved – your bill could also contain the loan repayments," thus making the payment process easier and automatic.

Overall, though, Dubuisson says that what needs to maintained is a strict adherence to standards: "Quality has to be taken back to the centre," he says. "We can move on to more stringent quality requirements but the main issue is training and certification of designers and installers."

In order to do this, Dubuisson proposes an official certification scheme: "The public can be confident about a recognised training and certification scheme."

Richard Douthwaite, while broadly in agreement with Dubuisson is cautious about interfering with the interest rate on offer: "I don't think the interest rate should be subsidised," he says. "Credit Unions can't offer differential rates. They have a policy that all people should be treated equally."

He does accept, however, that commercial lending organisations may approach things from a different perspective:

"With the banks, they might be prepared to lower the rate because the risk is lower," says Douthwaite, "The saved money [in energy and fuel costs] lessens the risk. Furthermore, as you're investing in the property you're actually increasing the value of the collateral."

Indeed here we can see two key reasons why banks may find such a scheme attractive. In September the UK lending institution Northern Rock was bailed out by the Bank of England, acting in its role as 'lender of last resort'. Quite apart from the possibility of similar conditions arising in Ireland, international financial markets are not only interconnected but also notoriously panic-prone, not to mention increasingly risk-averse. In the few days after the Northern Rock bailout the Irish stock market saw e7.5 billion wiped off its value.2

It appears that a full-scale credit crunch is a real possibility. For several months US economic journalist Doug Henwood has been tracking the so-called 'sub-prime' mortgage market and its effect on the overall economic health of the country. In the last few months this fringe research has become front page news. Meanwhile in Ireland it is widely promoted that while a crash is unlikely, the boom years for the building industry – and presumably mortgage lenders – have come to an end.

Although the current problems may be temporary, it is clear that right now is not a good time for lenders so, as Douthwaite indicates, lower-interest loans predicated on energy efficiency are good news for lenders: firstly, they are a low-risk loan as the savings can be translated directly into repayments for the duration of the loan period. Secondly, the improvements improve the resale value of the property, particularly in light of the introduction of BERs.

One possible mechanism for stimulating further interest among lenders would be to offer a government-backed guarantee that loans would be repaid, perhaps through a mechanism similar to the student loans system in countries including the United Kingdom and Canada. According to Douthwaite, however, this measure may not be of any particular interest to lenders "The Credit Unions wouldn't be interested in a guarantee – they don't work that way. They work on the basis of knowing people, it's the whole idea of a community bond."

Moreover, from the perspective of commercial lenders such as banks, a guarantee may simply be an irrelevance. Complex and thorough credit checking systems are already in place for vetting customers' ability to repay while the simple mechanics of the loan make it a good bet for the banks: a loan designed to significantly reduce energy costs in the home is perhaps the only lending that actually enhances the borrower's ability to repay. Put simply, less money spent on energy equals a greater ability to repay the capital while also enhancing the resale value of the home. In fact, such a scheme would be a rare example of loan that actually improves the borrower's ability to repay the capital borrowed.

Much like the Greener Homes scheme, the proposed loans could become a victim of their own success unless due care is given to controlling the rate of uptake. The worst-case scenario would be if the initial public response outweighed the ability of the Credit Unions and the independent energy experts to field the loan requests. It would inevitably take time to establish the optimum number of energy experts, and therefore the long-term success of the loans is to a large extent dependent on controlling the rate of growth to within manageable levels.

It’s also critical in terms of engendering consumer confidence in the loans, and the matter of cutting CO2 emissions as much as possible, that the people who initially take out the loans find it a positive experience in terms of the speed at which the whole process, from application, to initial BER assessment, to energy upgrade work, to final BER assessment, takes place.

A possible solution that would help to control the rate of growth of the loans, allow time to build capacity in terms of energy experts, and help ensure that the initial loans are successful, would be to include a restrictive requirement: homeowners should attend an energy awareness course, which might run to one or two days to learn the basics and ensure that they are more able both to make the right choice in terms of which materials or technologies they agree with the energy expert to install and, ultimately, ensure that the projected energy savings are actually achieved.

Such an approach would ensure that the people applying for loans in the first phase are genuinely interested in and committed to reducing energy consumption – and therefore more likely to ensure their upgraded homes perform as they should. It would also significantly help to heighten awareness about how to make homes energy efficient – which should in turn speed up the process for the energy experts when assessing what energy improvements to make in each house, without having to waste time explaining the different options every time. Crucially, it would help to restrict the number of people applying initially to manageable levels. As capacity grows, with more and more local independent energy experts becoming available, the energy awareness course could be transformed into an online course (although perhaps a conventional course option could be kept open for those who prefer it or without computers). This would help to reduce costs of delivering this information once the scheme is fully developed.

The second BER assessment, performed upon completion of the work, would ideally also satisfy the requirements of the Energy Performance of Buildings Directive (EPBD) in terms of providing a BER whenever a house is sold or rented. Therefore, this would remove the cost – circa e200 to e300 – of having a BER assessment carried out by the homeowner should they decide to sell or rent the property within 10 years of getting their loan.

Leading the way

There are international examples which Ireland can follow. Both the Netherlands and Austria, for instance, have instituted similar so-called 'soft loan' schemes. The Dutch scheme in particular was designed specifically to address the fact that despite growing interest in renewable energy technologies, fewer consumers understood the benefits of energy saving in the home.

In a recent interview with EPBD Building Platform, Teun P. Bokhoven, president of the Dutch renewable energy federation DE Koepel, argued that a loan can be devised to firstly address the low hanging fruit before moving on to other areas.3 Bokhoven also stated that any loan must "lead to a minimum 30 per cent energy reduction per household."

Administered through a public-private partnership at an interest rate of four per cent over a timeframe of fifteen years, the Dutch model is certainly one clear course of action that Ireland could follow. Alternatively, an agreement between the government, the lenders and the likes of the energy agencies could prove equally up to the task.

Regardless of which path the country follows, what is vital is that both the public and the industry know that the support is out there and that the public, in particular, can be confident about the independence of any advice they are given and the standards of any work performed. If growth in the sector and greater sustainability are the objectives then it is clear that some support is required.

As Xavier Dubuisson says: "The one thing that everyone in the renewable energy sector will tell you is that the government must be consistent in its support. When it [Greener Homes] was planned it was for five years. Stopping after two years is a big problem in itself. The fact that we're in this void at the moment rings a lot of alarm bells."

Xavier Dubuisson cautions that, no matter what the future of grant schemes such as Greener Homes or the proposed soft loans, a lassiez-faire attitude simply will not work: "If what happens is that the government was to step away from providing support, it would be a disaster. A free-market [approach] is not the solution for climate change. If you leave it all to the market forces you will not achieve the desired outcome. What is needed is clever financial mechanisms. "The big question is 'for how long?' I have no answer to that."

1Kane, C. Greener Homes move to result in job cuts, Irish Examiner, Cork, 11 September, 2007

2Staff reporter, UK Chancellor steps in to guarantee Northern Rock, Irish Independent, 18 September, 2007

3Staff reporter, Interview with Teun P. Bokhoven, EPBD Building Platform, June 2007

- Articles

- Energy Performance of Buildings Directive

- Green Loans

- economy

- renewable energy sector

- Greener Homes scheme

- Feasta

- douthwaite

Related items

-

Green shoots for green building

Green shoots for green building -

Embodied carbon & zero emission targets adopted in new EPBD

Embodied carbon & zero emission targets adopted in new EPBD -

EU votes through EPBD recast

-

Green loan rate for new HPI-certified housing

Green loan rate for new HPI-certified housing -

Green groups critical of latest budget

Green groups critical of latest budget -

Passive house costs falling, new study finds

Passive house costs falling, new study finds -

New housing should be to passive house standard — Climate Change Committee

New housing should be to passive house standard — Climate Change Committee -

Saint-Gobain launches free nZEB training courses

Saint-Gobain launches free nZEB training courses -

Green finance must be longterm & sustainable — Ecology

Green finance must be longterm & sustainable — Ecology -

England, Scotland & Wales will fail to meet ‘nZEB’

England, Scotland & Wales will fail to meet ‘nZEB’ -

New build homes face emerging ventilation crisis

New build homes face emerging ventilation crisis -

Dept of Housing set to launch new Part L for non-domestic buildings

Dept of Housing set to launch new Part L for non-domestic buildings